Are unicorns an endangered species? Unicorns, Venture CapitalJune 23, 2023397Views0Likes0CommentsWatch a panel at Viva Technology 2023 in Paris where VCs and entrepreneurs discuss if unicorns are a measure of success and a tool for innovation.Read More

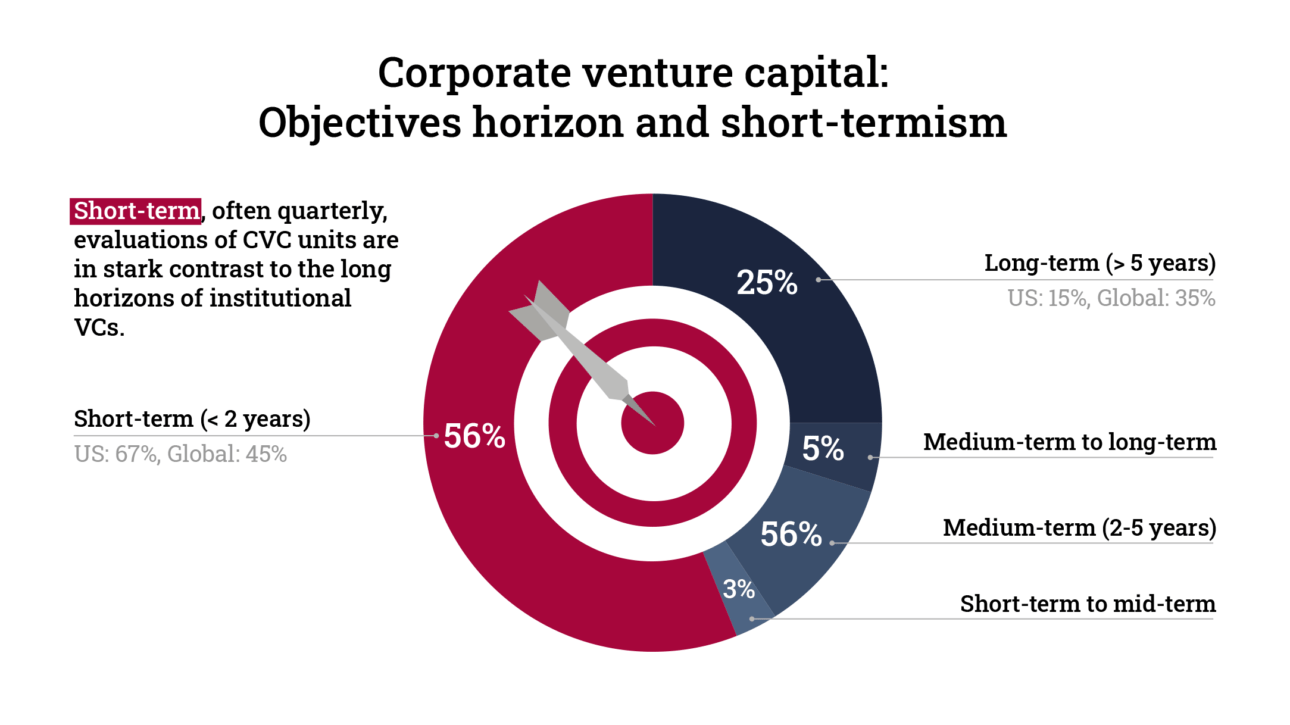

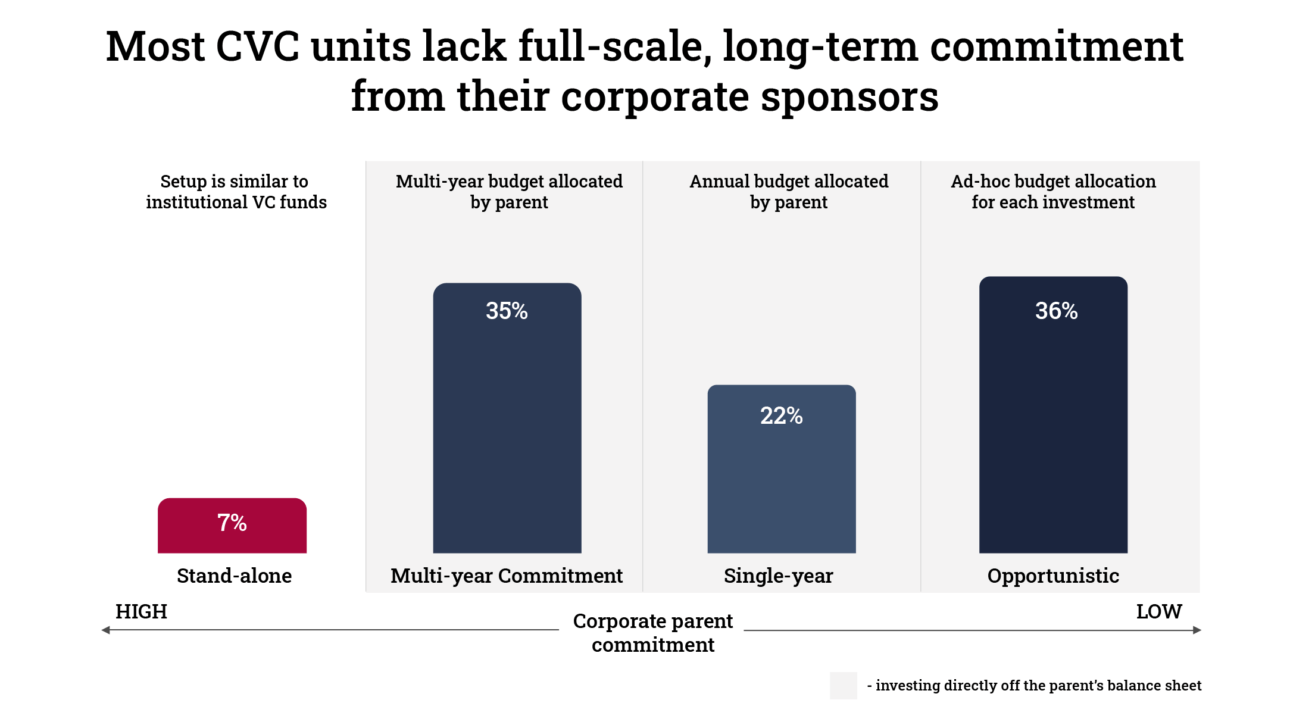

Is it good to have short-term goals? Venture CapitalApril 7, 2023435Views0Likes0CommentsThe results of the study covering 164 US and Global Corporate Ventures shows disturbing results.Read More

Decision making and success in corporate ventures CVC, Venture CapitalAugust 17, 2022404Views0Likes0CommentsA keynote speech and interview with Ilya Strebulaev on the results of a decade research.Read More

How do corporate VCs make decisions? Venture CapitalOctober 5, 2021417Views0Likes0CommentsA study by Ilya Strebulaev and Amanda Wang shows the pattern among CVCs.Read More

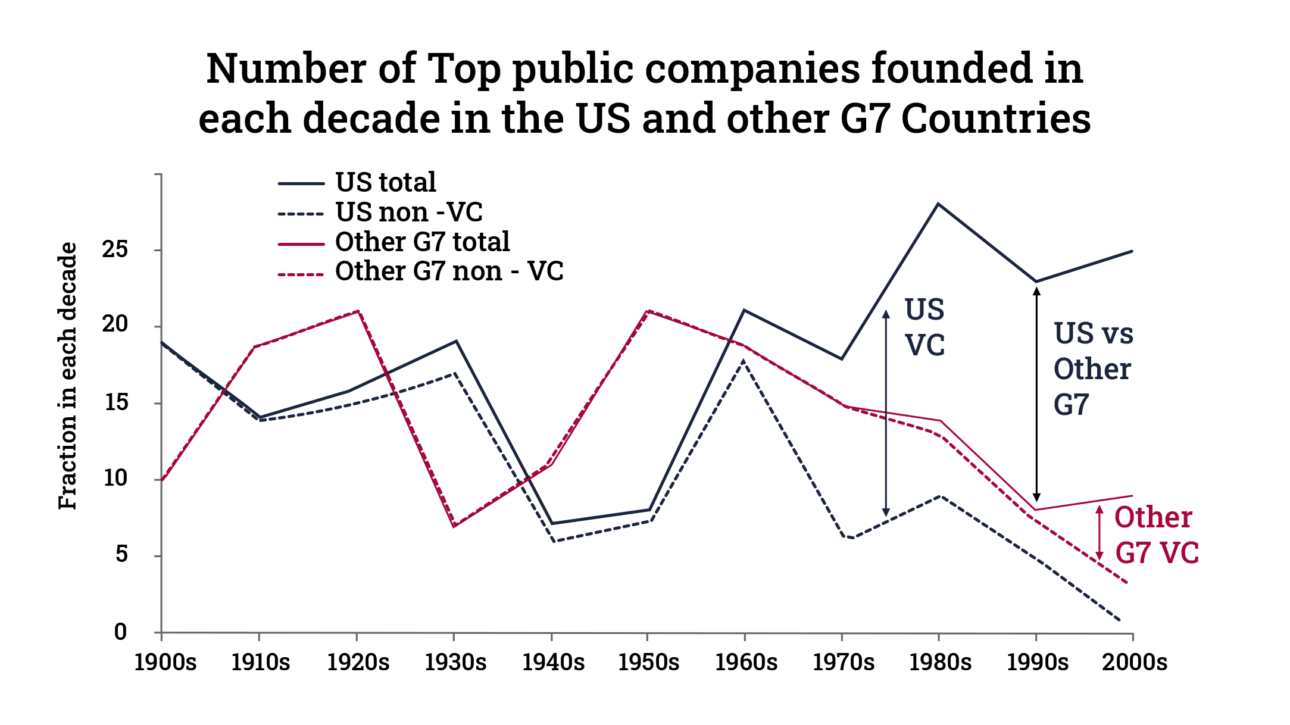

What is the economic impact of venture capital? Economic Impact, Venture CapitalAugust 3, 2021438Views0Likes0CommentsSome of the largest US companies would not have existed or achieved their current scale without VC.Read More