The key is to embrace risk, disagreement, and agility.

Big companies and risk capital can be awkward partners. Here’s how to get corporate venturing right.

Venture capitalists don’t mind strike-outs, so long as they get their home runs.

Finding and funding truly innovative ideas is a highly disciplined process.

What venture capitalists can teach us about working more efficiently.

How venture capitalists approach risk has lessons that apply beyond Silicon Valley.

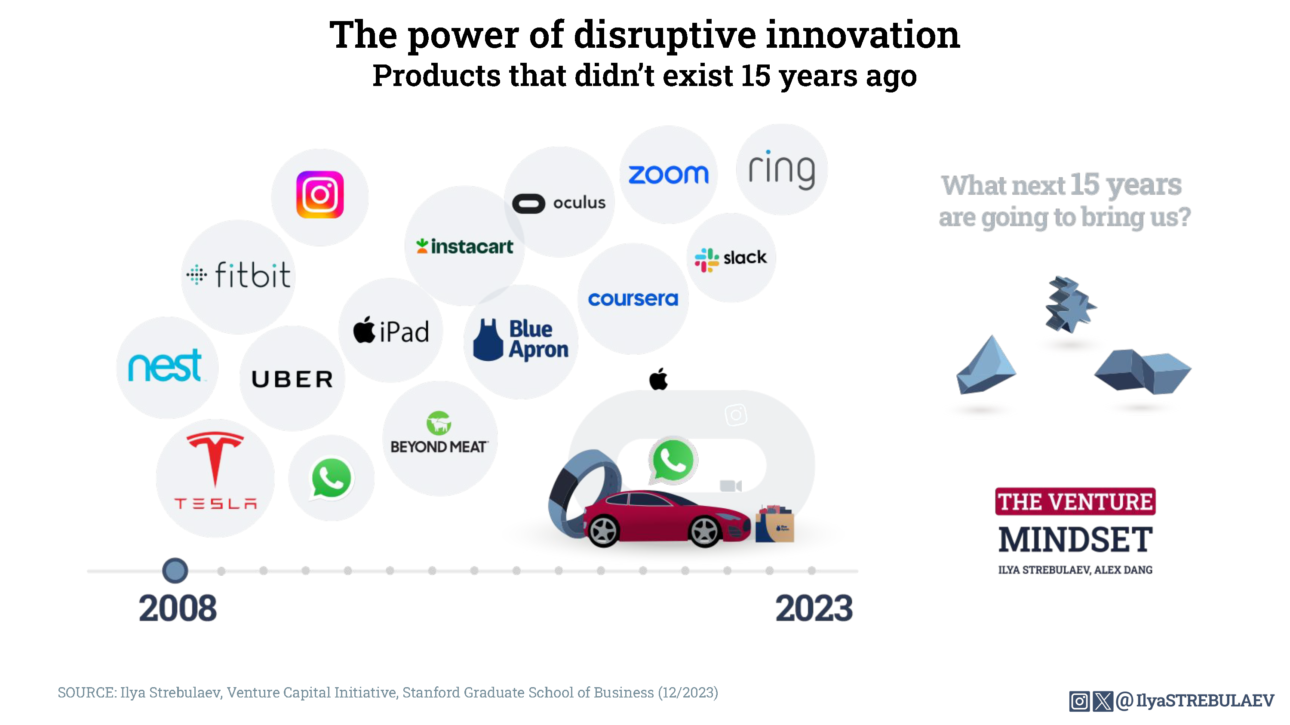

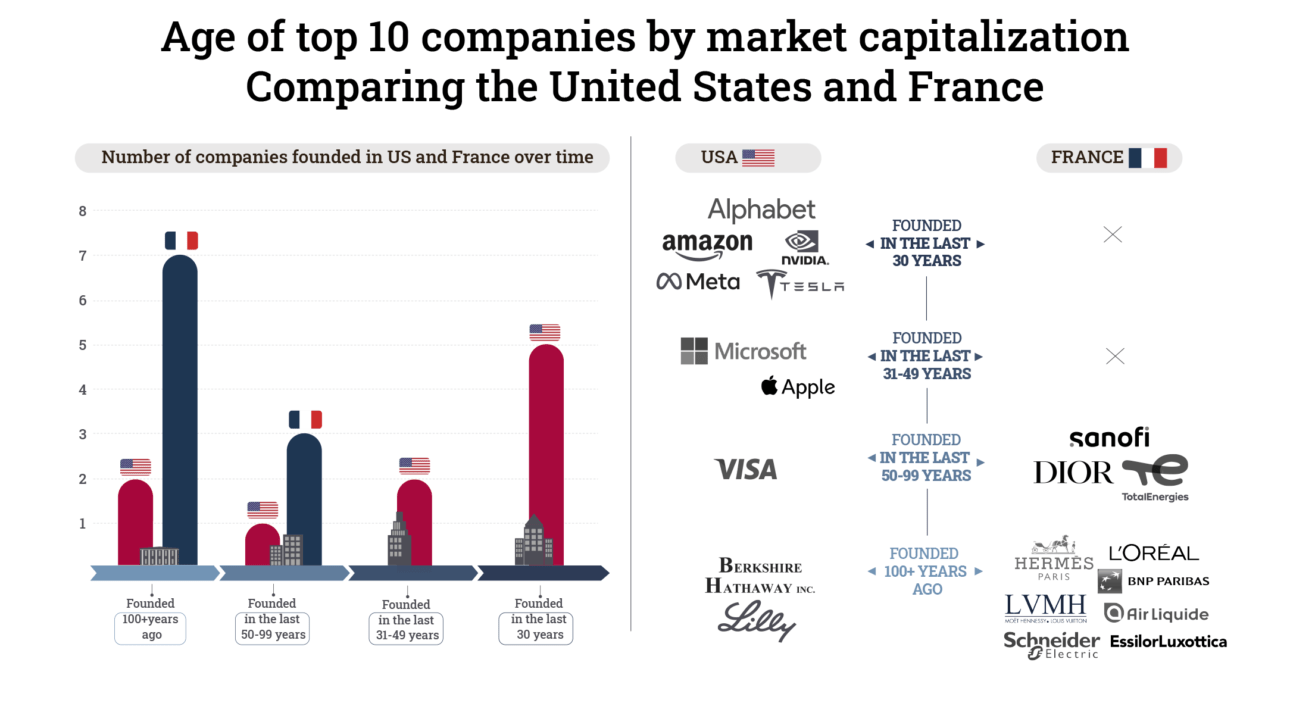

Many products that we use every day weren’t even around just 15 years ago.

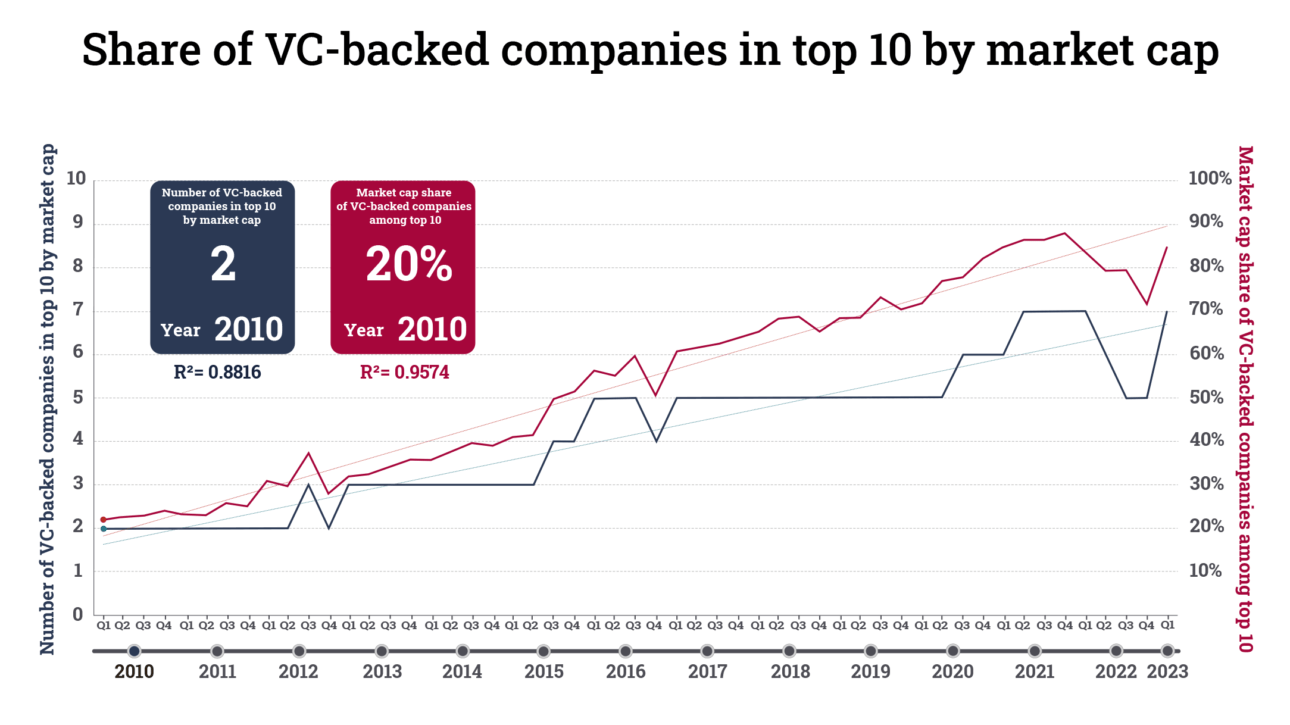

We identified the top 10 US companies by market cap over time and found the surprising pattern.

Watch the video to quickly learn the main points from Ilya Strebulaev’s Venture Capital course at Stanford.

Our findings on the major differences in entrepreneurship between the US and France.